Top Tax Filing Mistakes in 2025 That Are Triggering Notices for Indians

How One Small Tax Mistake in 2025 Can Cost You Refunds, Penalties & Peace of Mind

2026 is almost here, and tax season is looming for millions of Indians. For most, filing taxes is stressful, such as confusing forms, changing laws, deadlines, and the constant worry of making mistakes that could cost money or trigger notices. Every year, thousands of taxpayers fall into avoidable traps simply because they weren’t aware of some rules, overlooked deductions, or rushed the process. If you’ve ever wondered whether you’re paying too much tax or missing out on savings, this guide is for you. We’ve rounded up the top tax pitfalls in 2025, explained why they happen, and how you can avoid them, all in simple, practical language. By the end of this read, you’ll feel confident about filling your Income Tax Return (ITR) correctly and efficiently, and you’ll understand how platforms like taxufiling.com can make your life easier.

Ignoring Income Tax Act 2025 Changes: A Costly Filing Mistake for Indians

Tax rules are not static. The Indian government updates regulations every year, from GST adjustments to revised exemptions and deductions. Ignoring these updates is one of the biggest mistakes taxpayers make.

Many people assume that what worked last year will work again, but this can lead to missed deductions or even penalties. For instance, certain deductions under Section 80C have limits and thresholds that change based on government policy. Similarly, exemptions for capital gains or house property might have tweaks that you need to know.

How to avoid this: Stay informed. Follow credible sources for updates or use services like taxufiling.com, which automatically reflect the latest rules when preparing your ITR. Being proactive ensures that you don’t miss out on benefits and make costly mistakes.

Missing Out on Eligible Deductions

One of the most common pitfalls is failing to claim all eligible deductions. India offers multiple tax-saving opportunities under sections like 80C, 80D, and 80E. these include investments in PPF, ELSS, health insurance premiums, tuition fees, and home loan principal payments.

Many taxpayers either don’t know about these deductions or forget to claim them. Missing them can result in higher tax liability than necessary. For instance, if you didn’t claim your health insurance premium under 80D, that’s money you effectively lose.

Choosing the Wrong ITR Form

India has multiple ITR forms, each designed for different income types and categories of taxpayers. Choosing the wrong one is a common but serious mistake. Filling out an incorrect form can delay refunds, trigger notices, or even attract penalties.

For example, salaried individuals might think ITR-1 covers all income, but ig you have capital gains or rental income, you should opt for ITR-2 or ITR-3 depending upon your situation.

Tip: Double-check your income sources and match them to the appropriate ITR form. This reduces errors and ensures your filling is smooth.

Failing to Verify Your Return

Many taxpayers forget that filing their return is only half the process. E-verification is mandatory for the Income Tax Department to process your ITR. Without it, your filing is considered incomplete, and refunds can be delayed.

The good news is that e-verification is simple. You can do it using Adhaar OTP, net banking, or through your digital signature. But forgetting or delaying this step is a trap many fall into, especially at the last minute.

Solution: Verify your return immediately after filing. Automated platforms send reminders and guide you through verification so that your filing is completed without delays.

Missing Capital Gains Exemptions

Capital gains from property, stocks, or mutual funds are often misunderstood. Many taxpayers fail to account for exemptions that can significantly reduce tax liability. Without proper attention, you might end up paying more than necessary.

Tips to manage:

- Review all investment gains thoroughly.

- Check applicable exemptions under the Income Tax Act, including long-term capital gains exemptions.

- Platforms like taxuFiling.com automatically identify exemptions, making sure you only pay what’s due.

Walking Away from Refunds: Skipping TDS Claims

Imagine overpaying the government and never asking for your money back. That is what happens when taxpayers ignore TDS refunds. The reason? Either they don’t reconcile forms or assume the process is “too much hassle.”

Smart step: Check Form 26AS and AIS carefully. If your employer or bank deducted more than needed, file a refund claim. With taxuFiling.com, reconciliation is automatic, which means no missed refunds.

Your ITR must mirror the government’s records. Even a small mismatch between your declared income and data in Form 26AS or AIS can invite scrutiny. Notices are often triggered by these errors. The IT department already knows your numbers; however, the only question is, do you match them?

The Deadline Rush: Waiting Until the Last Minute

We’ve all witnessed it: the panic of the previous week, servers going down, people filling out forms in a hurry, and errors increasing. Not only can late filing result in fines of up to ₹5,000, but it also raises the possibility of mistakes.

Catchy idea: You shouldn’t wait for deadlines to arrive.

Smart move: Approach tax preparation similarly to studying for a test; the earlier you begin, the more assured you will be. Filing with TaxuFiling.com is accurate enough to allow you to rest easily and fast enough to complete early.

Records Matter More Than You Think

Think filing is the end? Not really. The tax department can ask for proof months or even years later. Without them, deductions may be disallowed, leaving you liable. A digital file today can save you from sleepless nights tomorrow. Keep electronic copies of your insurance premiums, investment proofs, FD certificates, and rent receipts. With such services online, everything is kept in one location and organized.

FAQ

1. What are the biggest tax mistakes Indians are making in 2025?

The most common mistakes include choosing the wrong ITR form, ignoring new tax rules, missing eligible deductions, failing to reconcile AIS/26AS, delaying e-verification, and rushing near deadlines. These lead to penalties, notices, and missed refunds.

2. How do I stay updated with tax rule changes in 2025?

Tax rules change every year. You can track updates through government portals, reliable financial websites, or use tax platforms like TaxuFiling.com, which automatically apply the latest rules while preparing your return.

3. Which deductions do taxpayers commonly miss?

Deductions often ignored include Section 80C investments (PPF, ELSS, LIC), Section 80D health insurance premiums, Section 80E education loan interest, and Section 24(b) home loan interest. Missing them increases your tax outflow.

4. How do I choose the correct ITR form for 2025 filing?

Match your income sources to the correct form:

- ITR-1 for salaried individuals with simple income

- ITR-2 if you have capital gains or multiple properties

- ITR-3 if you have business income

Choosing the wrong form can delay refunds or invite notices.

5. Why is AIS/26AS reconciliation so important?

Your ITR must match the income reported in AIS and Form 26AS. Even small mismatches—for example, interest income or TDS from banks—can lead to scrutiny notices. Platforms like TaxuFiling.com automatically reconcile your data.

6. What happens if I forget to E-Verify my ITR?

Your return is considered invalid until it’s verified. Refunds won’t be processed, and you may need to refile. E-verification through Aadhaar OTP, net banking, or DSC is mandatory.

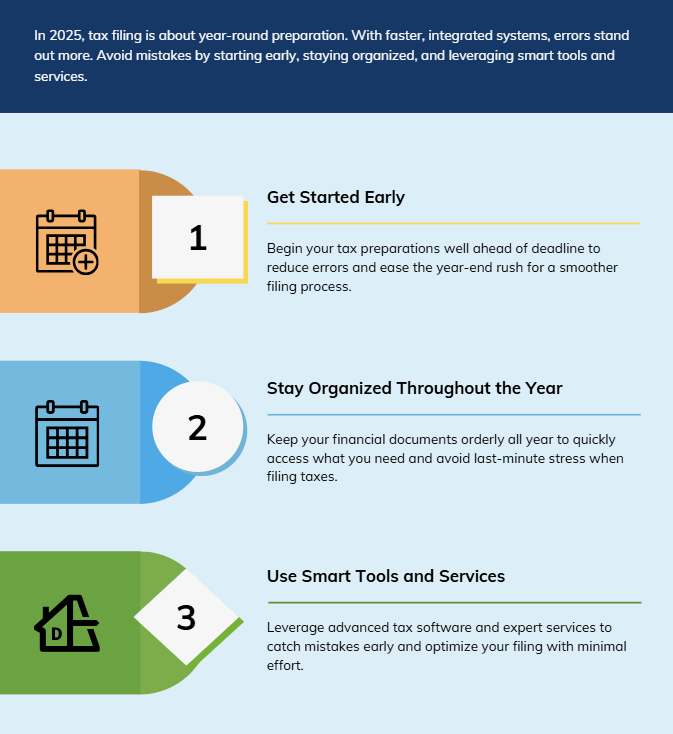

Final Takeaway: Filing Smarter in 2025

In 2025, paying taxes is more about being proactive throughout the year than it is about “filing once a year.” Errors are more noticeable because government systems are more integrated, computerized, and speedier.

The good news? It’s easier than ever to avoid these errors if you:

- Get started early

- Maintain organization

- Use smart tools and services

Bottom line: Avoid letting tax season deplete your finances or mental well-being. Make better filing decisions, maintain compliance, and retain more of your profits where they belong: with you.